Pakistan looks to end fiscal year on a high

Pakistan’s Fiscal Performance in 3QFY24

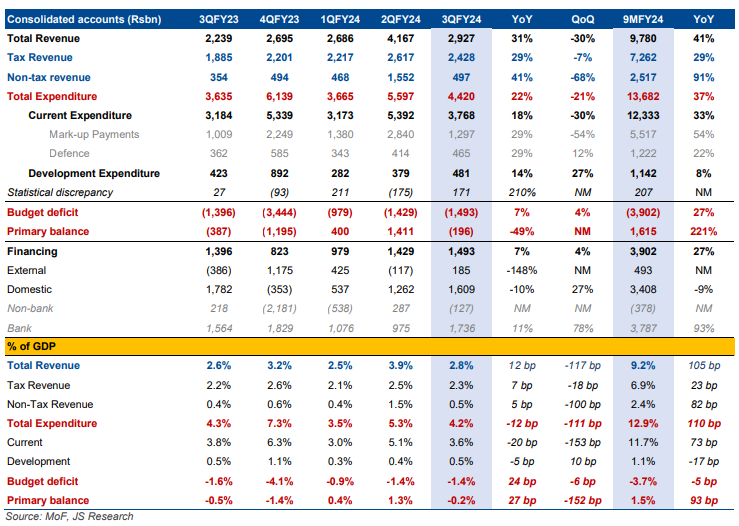

The Ministry of Finance has released fiscal accounts revealing a slip in the third quarter of FY24. The budget deficit reached 1.4% of GDP, higher than the 9-month FY24 average of 3.7% of GDP. Particularly concerning is the primary balance, which showed a deficit of 0.2% of GDP in the same quarter, reducing the 9-month primary surplus to 1.5% of GDP. This deterioration was mainly attributed to lower tax collection and the absence of State Bank of Pakistan (SBP) profits during this period.

Outlook for 4QFY24

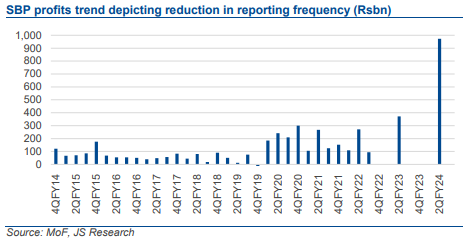

Attention now shifts to the fourth quarter of FY24. Despite the recent setbacks, there’s optimism about achieving a primary surplus for the first time in 20 years (last seen in FY04). The return of SBP profits, which are currently at record highs due to elevated Open Market Operations (OMO) levels, could significantly boost this prospect. SBP profits are anticipated to be reflected unevenly across quarters in fiscal accounts.

Implications of a Primary Surplus

Realizing a primary surplus would be a significant positive for market sentiment, especially considering its importance in meeting IMF program targets. However, risks remain, such as potential further slippages in tax collection or higher-than-expected expenditures, which could erase the chances of achieving a primary surplus.

Sequential Deterioration in Fiscal Performance

The fiscal position in Pakistan worsened sequentially in 3QFY24. This was primarily due to a 7% quarter-on-quarter (QoQ) decline in tax collection and the absence of SBP profits. Direct taxes and sales tax both experienced an 8% QoQ drop. Despite these challenges, mark-up expenses decreased seasonally, and subsidy spending saw a significant reduction of 74% QoQ, easing the burden on the government’s budget.

Path to a Primary Surplus

Pakistan’s tax collection for 10MFY24 has fallen short of targets, with monthly collections consistently below expectations. However, the reliance on SBP profits has softened concerns. Non-tax revenue has reached 85% of the annual budgeted figures for FY24.

Projections for 4QFY24

Assuming no QoQ growth in total revenue and factoring in expected mark-up expenses and other expenditure increases, the estimated fiscal deficit for 4QFY24 could be 3.6%, with a primary deficit of 0.6%. Despite a potential miss in the FY24 fiscal deficit target, there’s a possibility of achieving a primary surplus of 0.9%—the first in two decades. Prospective SBP profits in 4QFY24 could further improve these projections.

Factors Driving High SBP Profits

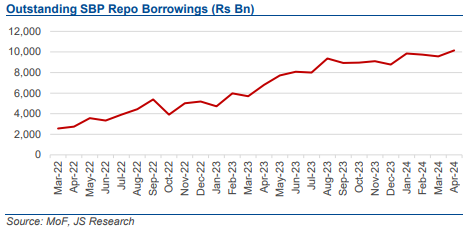

The increase in SBP profits this year is primarily attributed to a 50% surge in repo borrowings extended to banks and financial institutions. This rise is a response to the government’s fiscal requirements and the attractiveness of risk-free government securities’ yields, especially in anticipation of potential monetary easing measures. However, the sustainability of these profits is linked to the level of outstanding repo borrowings.

Disclaimer:

The information in this article is based on research by JS Research. All efforts have been made to ensure the data represented in this article is as per the research report. This report should not be considered investment advice. Readers are encouraged to consult a qualified financial advisor before making any investment decisions.

⚠️ This post reflects the author’s personal opinion and is for informational purposes only. It does not constitute financial advice. Investing involves risk and should be done independently. Read full disclaimer →

Leave a Reply