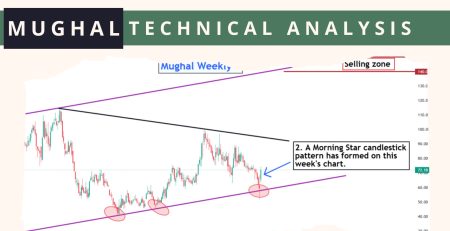

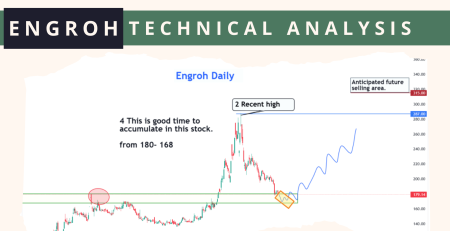

A look at EFERT’s bullish thesis

As Pakistan enters FY26, investors are closely eyeing the top-performing sectors poised to lead the market. Among the most attractive are energy, banking, and fertilizers—each offering a mix of earnings visibility, dividend potential, and macro-driven tailwinds. The energy sector stands to benefit from elevated oil prices and improved payout trends, while banks are set to gain from sustained high interest rates and robust deposit growth. Meanwhile, fertilizer companies are positioned for earnings growth on stable urea demand and favorable pricing. Together, these sectors form a compelling core for portfolio strategies in FY26.

Sector overview:

Pakistan’s fertilizer sector is showing strong signs of recovery, with profitability expected to grow by 25% year-on-year in the second quarter of 2025. This surge is driven by higher product sales across key nutrients. Sales of Urea, DAP, CAN, and NP fertilizers have risen by 3%, 12%, 56%, and 19% respectively. What’s fueling this demand? Three things: fertilizer companies offered discounts, farmers had access to interest-free loans through the Punjab Kisan Scheme, and many dealers and farmers bought fertilizers just in time as stock levels were running low earlier in the year. As a result, companies are also seeing improved profit margins, expected to rise to 35.6% this quarter. Dividend payouts are also expected to grow by 21%, keeping pace with earnings. Among all this activity, Engro Fertilizers (EFERT) stands out with the strongest earnings rebound.

📢 Announcement: You can now access our services and similar analyses by opening an account with us via JS Global

Company overview: Engro Fertilizers (EFERT)

EFERT is one of the key players in Pakistan’s fertilizer industry, and the second quarter of 2025 looks like a big comeback for the company. After facing higher costs last year due to a temporary plant shutdown, EFERT is now expected to post a massive 3.5x jump in earnings, reaching PKR 5.8 billion in profit (EPS: PKR 4.4), compared to PKR 1.7 billion (EPS: PKR 1.25) during the same time last year.

This turnaround is largely thanks to increased sales volumes. Urea offtake rose to 431,000 tons from 307,000 tons last year, and DAP sales increased by 33% year-on-year. The company’s total revenue is projected at PKR 53.4 billion, up 35% from the same quarter in 2024. Gross margins, a key measure of profitability, are also set to improve significantly, jumping from 18.1% to around 31%. Even though other income is likely to fall due to fewer investments and finance costs remain elevated, the overall earnings growth paints a positive picture.

Financial snapshot

| Metric | EFERT (2QCY25E) | EFERT (2QCY24) | YoY Change |

|---|---|---|---|

| EPS (PKR) | 4.5 | 1.2 | +260% |

| DPS (PKR) | 4.5 | 3.0 | +50% |

| Target Price (PKR) | 28.39 | – | – |

| Current Price (PKR) | 28.09 | – | – |

| P/E (x) | 6.6 | 6.7 | -1% |

| P/B (x) | 5.8 | 5.8 | – |

| Dividend Yield (%) | 14% | 15% | -1% |

Why are analysts bullish on EFERT?

Analysts are positive on EFERT due to the sharp recovery in earnings and improvement in gross margins. The company has bounced back from last year’s plant shutdown, and sales growth has been impressive, particularly for Urea and DAP fertilizers. Despite some pressure on other income and financing costs, the core business has become more profitable. Margins are normalizing, sales are growing, and EFERT continues to pay out strong dividends. In fact, a 100% payout ratio is expected for this quarter, with analysts forecasting a cash dividend of PKR 4.5 per share. With a projected EPS of 6.7 for the half-year, EFERT has outpaced most peers in growth momentum.

Risks to watch

📢 Announcement: We're on WhatsApp – Join Us There!

Despite the upbeat outlook, there are some risks investors should keep in mind. First, the fall in other income due to reduced investment returns may limit overall profitability in future quarters. Second, financing costs remain elevated because of higher working capital needs and inventory levels. Lastly, while EFERT is seeing strong offtake this quarter, sustainability of sales momentum depends on continued farmer demand and government support measures like the Punjab Kisan Scheme. Any reversal in these factors could pressure margins and cash flows.

Engro Fertilizers is clearly leading the pack in terms of earnings growth this quarter. With sales volumes rising, margins improving, and dividends staying strong, EFERT stands out in the fertilizer sector for CY25. However, keeping an eye on borrowing costs and investment income trends will be key to assessing the stock’s performance in the quarters ahead.

⚠️ This post reflects the author’s personal opinion and is for informational purposes only. It does not constitute financial advice. Investing involves risk and should be done independently. Read full disclaimer →

Leave a Reply