Insight Securities upgrades BAFL price target to Rs. 74

Insight Securities has just released an update on its coverage of Bank Alfalah Limited (BAFL). The research house has raised its Dec 24 BAFL price target to Rs. 74 per share.

Here are the key points from the report:

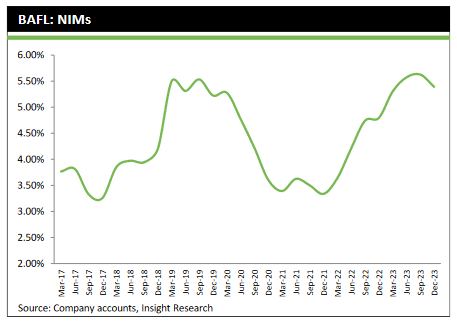

In recent years, Bank Alfalah Limited (BAFL) has demonstrated significant growth in deposits, surpassing industry averages. This momentum shows the bank’s resilience and potential for investors. Furthermore, BAFL’s profitability has witnessed a notable surge, doubling year-on-year. This upturn can be attributed to both increased volume and favourable interest rates, enhancing the bank’s net interest margins (NIMs).

The expansion of BAFL’s branch network has been instrumental in driving its deposit growth. With a focus on prudent lending practices, technological advancements, and consistent dividends, BAFL presents an enticing investment proposition. Currently, BAFL is trading at attractive valuations, with a forward price-to-earnings (P/E) ratio of 2.1x and a price-to-book (P/B) ratio of 0.5x.

Key Investment Highlights:

- Deposit Growth: BAFL has achieved remarkable deposit growth, positioning itself as the 5th largest bank in Pakistan. The bank’s aggressive branch expansion strategy has been a significant driver of this growth, with plans for further expansion in the future.

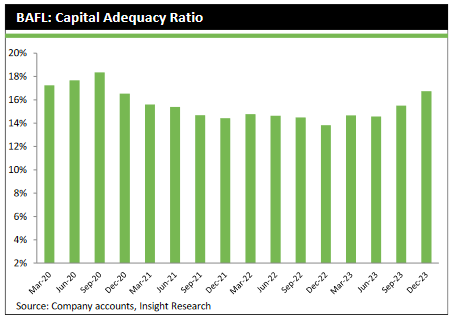

- Profitability: BAFL’s profitability has been bolstered by its deposit growth strategy and prudent lending practices. Despite economic challenges, BAFL maintains a healthy capital adequacy ratio (CAR) of approximately 16.7%.

- Lending Policy: BAFL has adjusted its lending policy to mitigate risks amidst macroeconomic uncertainties. The bank has reduced its high advance-deposit ratio (ADR) and diversified its income streams through investments in treasury bills (T-bills) and Pakistan Investment Bonds (PIBs).

- Dividends: BAFL pays dividends to its shareholders, and the bank is considering paying them more often.

Investment Thesis:

Insight Securities maintains a BUY recommendation on BAFL with a target price of PKR74/sh by December 2024, offering a potential capital upside of 41% and an attractive yield of 15%. However, it’s essential to acknowledge the associated risks, including lower-than-expected deposit growth, higher operating expenses, economic volatility, and regulatory changes.

In summary, Bank Alfalah Limited presents a compelling investment opportunity driven by its robust deposit growth, prudent lending practices, and attractive valuation. With a focus on expansion and profitability, BAFL is well-positioned for sustained growth in the Pakistani banking sector.

⚠️ This post reflects the author’s personal opinion and is for informational purposes only. It does not constitute financial advice. Investing involves risk and should be done independently. Read full disclaimer →

Leave a Reply