SBP Hikes Rate 100bps to 11.5%

| PSX INVESTMENT ANALYSIS · APRIL 28, 2026 SBP Hikes Rate 100bps to 11.5% Winners, Losers, and What Smart Money Does Next By Nagina Akram | KSE-100 Sector Research | Policy Rate Analysis |

AT A GLANCE — KEY NUMBERS

| NEW POLICY RATE | PREVIOUS RATE | SHORT-TERM INFLATION | SAUDI DEPOSIT USD 3B |

|---|---|---|---|

| 11.50% +100 bps overnight | 10.50% Held since March 9 | 14.0% Week of Apr 23, 2026 | Received Apr 15 + 20 |

The Shock Move No One Wanted But Everyone Saw Coming

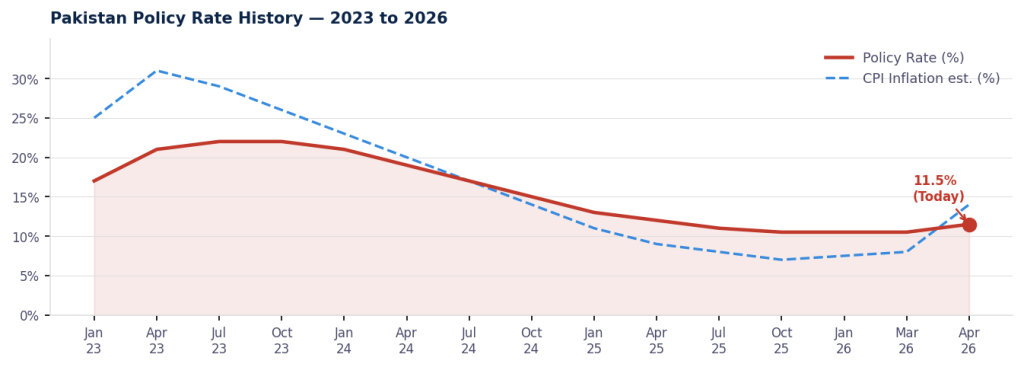

Yesterday, the State Bank of Pakistan (SBP) delivered one of the sharpest single monetary policy decisions of 2026 — a 100 basis point hike in the policy rate, pushing it from 10.5% to 11.50%, effective April 28, 2026.

If you were hoping for a rate cut this cycle, the Middle East just killed that dream.

The Monetary Policy Committee, chaired by SBP Governor Jameel Ahmed, cited escalating geopolitical tensions — specifically the Iran-US conflict — as the primary driver. Global oil prices have surged. The Strait of Hormuz, through which a significant share of the world’s oil passes, remains under pressure. And Pakistan, an import-dependent economy, cannot absorb an oil price shock without feeling it directly in inflation, the current account, and the rupee.

The SBP did not blink. It hiked — hard and fast.

This article does what most news coverage won’t: it tells you exactly which PSX sectors bleed from this decision, which ones quietly benefit, and where a disciplined investor should be positioning right now.

PAKISTAN POLICY RATE HISTORY — 2023 TO 2026

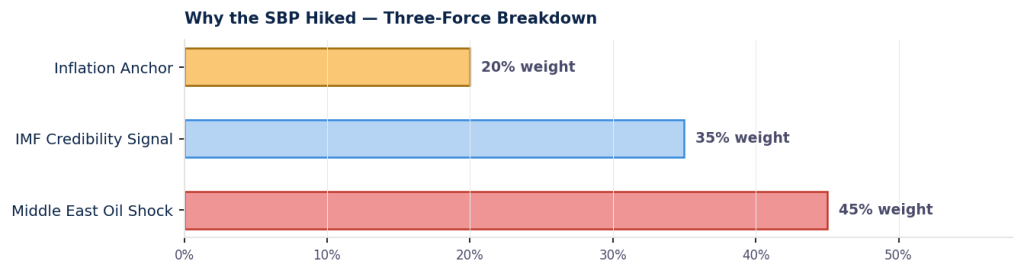

Why the SBP Pulled the Trigger — Three Forces at Work

Understanding the why behind this hike is essential before making any investment move. This was not panic. It was calculated. Three forces converged simultaneously.

1. The Middle East Energy Shock

The Iran-US war has disrupted global energy supply chains in ways that are not going away in the next few weeks. Oil prices have climbed sharply, and freight and insurance costs for Pakistan’s imports are running above normal levels. When fuel prices rise, the impact is not limited to petrol pumps — it passes through to every single good that moves on a truck, every factory that runs on diesel, and every household cooking on gas.

Pakistan is particularly vulnerable because it imports a large portion of its energy needs. Short-term inflation hit 14% for the week ending April 23, 2026 — a sharp warning signal that the SBP could not ignore without risking a wage-price spiral.

2. The IMF Deadline

This is the angle most commentators have missed. The IMF Executive Board meets on May 8, 2026 to consider approving more than $1.2 billion in fresh disbursements — roughly $1 billion under the $7 billion Extended Fund Facility, plus $210 million through the Resilience and Sustainability Facility. A rate hold with inflation rising would have sent entirely the wrong signal to Washington. The SBP’s hike is, in part, a message to the IMF: we are managing this responsibly.

This is good news for external account stability. If the May 8 board approval goes through, total IMF disbursements will reach approximately $4.5 billion.

3. The Saudi Cushion

Pakistan is not walking into this tightening cycle without a safety net. Saudi Arabia deposited $3 billion with the SBP — $2 billion on April 15 and $1 billion on April 20. This has materially strengthened foreign exchange reserves and given the SBP the confidence to tighten without triggering a currency crisis. The rupee is not in freefall. That changes the calculus for equity investors significantly.

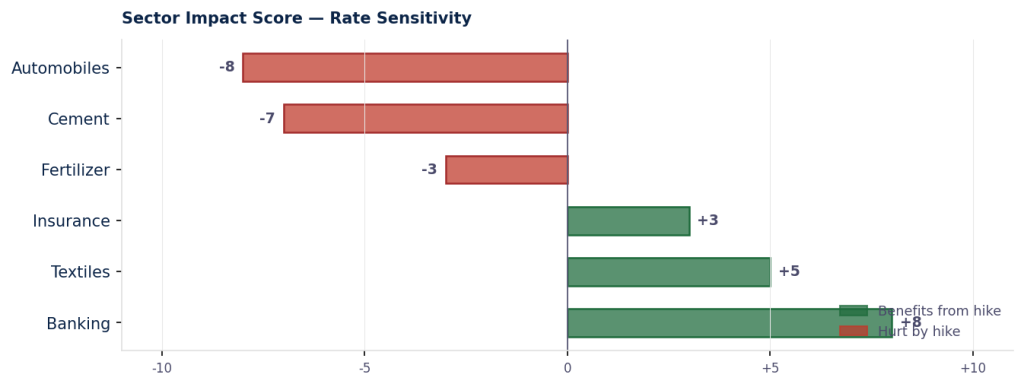

The PSX Sector Scorecard: Who Wins, Who Loses

This is the section that matters for your portfolio. Rate hikes are not uniformly bad for stocks — they create a powerful rotation from borrowers to lenders, from leveraged businesses to cash-rich ones.

| Banking | MCB · HBL · MEBL · UBL · ABL | STRONG BUY | NIMs expand as loans reprice faster than deposits. T-bill/PIB yields rise immediately. Best rate-hike trade on PSX. |

| Textile Exporters | NML · Interloop · Nishat Mills | BUY | Dollar revenues, rupee costs. Protected by export refinance facility. Any PKR weakness is additional upside. |

| Insurance | Jubilee · EFU · Adamjee | HOLD | Fixed-income investment portfolios earn higher yields as rates rise. Quiet, steady beneficiary. |

| Fertilizer | ENGRO · FFC · EFERT | HOLD | Working capital costs rise on top of gas pricing headwinds. Urea demand stays inelastic — volumes hold. |

| Cement | LUCK · MLCF · CHCC · DGKC | AVOID | Heavy debt reprices upward overnight. Construction slows. Finance costs will compress EPS in June results. |

| Automobiles | PSMC · HCAR · INDU | AVOID | Heavy debt reprices upward overnight. Construction slows. Finance costs will compress EPS in the June results. |

Top Stock Ratings — 12-Month Investment View

Based on the sector analysis above, here are specific stock-level ratings with the rationale behind each call.

| MCB Bank Commercial Banking STRONG BUY Strongest NIM expansion play on PSX. High CASA ratio, disciplined balance sheet, consistent dividend payer. The cleanest rate-hike trade. | HBL Commercial Banking BUY Largest private bank by assets. Significant government securities portfolio — rate hike is directly accretive to earnings. | Meezan Bank Islamic Banking BUY Pakistan’s largest Islamic bank. Loyal deposit base, strong CASA. Behaves like conventional banks in rate hike cycles. |

| Lucky Cement Cement HOLD Highest quality cement name — will weather headwinds better than peers. Hold and watch the June results. Re-rating candidate when rates reverse. | INDU / HCAR Automobiles AVOID Volume downside risk as consumer financing costs rise. Do not catch a falling knife here. Wait for the rate reversal signal. | INDU / HCAR Automobiles AVOID Volume downside risk as consumer financing costs rise. Do not catch a falling knife here. Wait for rate reversal signal. |

The Economic Outlook: What Comes Next

The SBP’s move is not the end of the story — it is the beginning of a new phase.

The inflation trajectory will be the key variable to watch over the next 6-8 weeks. If oil prices stabilise — or if the Iran-US conflict shows early signs of de-escalation — inflationary pressure will ease. Pakistan’s headline CPI will likely spike in the May and June prints before moderating.

The IMF board meeting on May 8 is a near-term catalyst. If the $1.2 billion disbursement is approved — which looks likely given the staff-level agreement in March — it will boost sentiment significantly. Combined with the $3 billion Saudi deposit, Pakistan’s reserves will be materially stronger.

The rate reversal scenario — this is the trade that serious investors need to be thinking about right now. The moment the MPC signals a pause or a cut — possibly as early as Q3 2026 — the market will reprice aggressively. Sectors that suffered most (cement, autos) will bounce sharpest.

The investors who will make money from this cycle are not the ones who react after the pivot — they are the ones who position before it.

WHAT TO WATCH — UPCOMING CATALYSTS

| Apr 28, 2026 | Rate effective today | KSE-100 likely tests support this week. Expect a 2–4% dip. That selloff is a buying opportunity in quality bank stocks — not a reason to panic sell. |

| May 8, 2026 | IMF board meeting | Expected to approve $1.2B disbursement. Approval = significant positive sentiment catalyst and may trigger a KSE-100 relief rally. |

| May–Jun 2026 | CPI inflation prints | If CPI peaks and starts easing, the rate reversal narrative begins to build. Cement and auto stocks start pricing in recovery before it happens. |

| Jun 2026 | Quarterly results season | Watch the finance cost lines in the cement sector results. Watch the NIM expansion in bank numbers. Data validates or challenges this thesis. |

| Q3 2026 | Possible rate reversal | If oil prices stabilise and tensions ease, SBP may pause or cut. This triggers the sharpest PSX rally of 2026. Be positioned before it — not after. |

The Action Plan: What to Do This Week

Here is a practical framework for different investor types. Be direct. Be disciplined.

| Conservative Investor | Growth Investor | Short-Term Trader |

|---|---|---|

| Rotate into dividend-paying bank stocks — HBL, MCB first | Accumulate quality bank stocks on any post-hike dip this week | Watch KSE-100 at 115,000 support level closely this week |

| Reduce exposure to companies with high debt-to-equity ratios | Start a small position in LUCK for the rate-reversal trade | Banks leading a bounce from support = bullish confirmation |

| T-bills and PIBs now yield attractively — park idle cash here | Watch textile exporters for PKR weakness as entry signal | Avoid cement and autos until next MPC direction is clear |

The Bottom Line

The SBP’s 100 basis point hike is a bold, necessary move made under exceptional circumstances. A Middle East war, rising global energy prices, an IMF programme deadline, and the need to anchor inflation expectations all pointed in one direction — tighter monetary policy.

For PSX investors, this is not a time for paralysis. It is a time for rotation. The money that flows out of rate-sensitive borrowers flows into rate-benefiting lenders. That trade — from cement and autos into banks — is the central investment thesis for the next two quarters.

The bigger opportunity, however, is setting up for the rate reversal. When the SBP eventually pivots — and it will, once inflation is contained and global energy markets stabilise — the KSE-100 will rally sharply. The investors already positioned in quality stocks across sectors will benefit most.

Stay patient. Stay disciplined. And watch that May 8 IMF board meeting very closely.

Follow this column for weekly PSX sector analysis, share price targets, and economic outlook updates. All views expressed are the author’s own based on publicly available data and are for informational purposes only.

| DISCLAIMER This article is for informational and educational purposes only. It does not constitute formal investment advice or a solicitation to buy or sell any securities. All views are the author’s own based on publicly available data as of April 28, 2026. Past performance does not guarantee future results. Readers should consult a SECP-licensed investment advisor before making financial decisions. Data: State Bank of Pakistan · Pakistan Stock Exchange · IMF press releases · Saudi Press Agency · April 2026 |

⚠️ This post reflects the author’s personal opinion and is for informational purposes only. It does not constitute financial advice. Investing involves risk and should be done independently. Read full disclaimer →

Leave a Reply