Insight Securities has just released an update on its coverage of Bank Alfalah Limited (BAFL). The research house has raised its Dec 24 BAFL price target to Rs. 74 per share.

Here are the key points from the report:

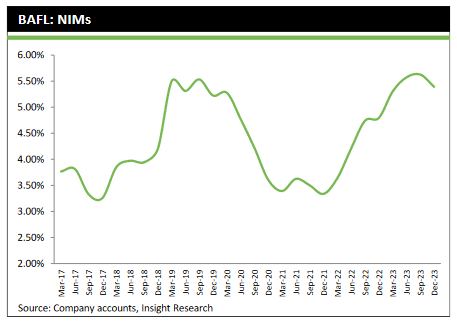

In recent years, Bank Alfalah Limited (BAFL) has demonstrated significant growth in deposits, surpassing industry averages. This momentum shows the bank’s resilience and potential for investors. Furthermore, BAFL’s profitability has witnessed a notable surge, doubling year-on-year. This upturn can be attributed to both increased volume and favourable interest rates, enhancing the bank’s net interest margins (NIMs).

The expansion of BAFL’s branch network has been instrumental in driving its deposit growth. With a focus on prudent lending practices, technological advancements, and consistent dividends, BAFL presents an enticing investment proposition. Currently, BAFL is trading at attractive valuations, with a forward price-to-earnings (P/E) ratio of 2.1x and a price-to-book (P/B) ratio of 0.5x.

Insight Securities maintains a BUY recommendation on BAFL with a target price of PKR74/sh by December 2024, offering a potential capital upside of 41% and an attractive yield of 15%. However, it’s essential to acknowledge the associated risks, including lower-than-expected deposit growth, higher operating expenses, economic volatility, and regulatory changes.

In summary, Bank Alfalah Limited presents a compelling investment opportunity driven by its robust deposit growth, prudent lending practices, and attractive valuation. With a focus on expansion and profitability, BAFL is well-positioned for sustained growth in the Pakistani banking sector.

On 20-02-2025, Lotte Chemical Pakistan Limited (LOTCHEM) disclosed the following material information.

On the monthly time frame, Netsol has a history of boom and bust cycles

OIL & GAS EXPLORATION COMPANIES (OGDC) have made good corrections but it is still in…

The Board of Directors of Lotte Chemical Corporation, South Korea (LCC Korea), the majority (75.01%)…

After the completion of the expected life of the furnace, Ghani Global Glass Limited (GGGL)…

Pakistan State Oil (PSO) is trying to sustain above 300 level.

{kind=link}